S.A. Istomin, Candidate of Engineering, CEO, Central Scientific Research Design Institute for Modern Technologies in the Valve Engineering Industry (OOO TSNIPI STARK), Moscow

Development of the Russian valve engineering for energy, same as that of any other sector or subsector of engineering, depends, on the one hand, on the condition of the industry that is the primary user of its products (in this case, nuclear and conventional energy), quantitative and qualitative goals pursued by the energy industry and, on the other hand, on the condition of businesses (manufacturing companies, design companies, testing facilities) involved in the manufacture of valves for the energy industry.

Analysis of the state of electric energy industry in Russia

Total installed capacity of power plants in Russia is 220,000 MW.The installed capacity of the operating power plants is structured as follows by type of generation:21% are hydroelectric power plants, 11% are nuclear power plants, and 68% are thermal power plants.

The long-term development of the electric energy industry in the Russian Federation is guided by the Master Plan of Energy Projects 2020.

Thermal energy

The dominance of thermal energy is a traditional and economically justified development pattern of the Russian energy sector.

Currently, the total installed capacity of cogeneration units is 154,700 MW.

According to the Roadmap of the Russian Thermal Energy Industry, 34,440 MW of new generation capacity will be commissioned in 2011 – 2017.

Given that about 50% of the generating capacity in the thermal energy industry require either replacement or retrofitting and upgrading due to obsolescence, it is reasonable to expect stable or moderately rising demand for valves for thermal power plants in the mid-term till 2020.

Valve markets for thermal and nuclear energy industries have certain similarities (similar parameters of working media, functionality, volume requirements, steel grades used, research intensity, testing complexity), but also fundamental differences in many respects:

- Full decentralization of thermal power generation market, in contrast to nuclear power.

- Large number of thermal power projects – depending on the fuel type, configuration, and power ratings of turbines and boilers.In nuclear energy, there are, generally speaking, only 2 relevant projects and 2 in the commissioning phase.

- Tighter operating conditions in terms of the working environment parameters, environmental standards, etc.

- Russia’s reliance on imports is over 50% in key process equipment for new projects (turbines, boilers, pumps).Before 1998, Russia was a country exporting technology and building thermal power plants abroad; it was almost independent of imports.Currently, Russia is a major importer of technology and equipment for thermal power industry.

- Design and technological dependence not only on general designers, but also to a large extent on the design of boilers and turbines, and hence on boiler and turbine plants.

Table 1. Analysis of reliance on imports of key generating equipment in the construction and upgrades (reconstruction) of thermal power plants*

| Parameter | Total capacity, MW | Share, % |

|---|---|---|

| Total, capacity commissioned/being commissioned, | 21593 | 100,00 |

| including: | ||

| gas units | 16174 | 74,90 |

| coal units | 5419 | 25,10 |

| including: | ||

| - based on gas turbines | 16 174 | 100,00 |

| including: | ||

| imported | 12 824 | 79,29 |

| manufactured in Russia | 3 350 | 20,71 |

| - based on steam turbines | 18 717 | 100,00 |

| including: | ||

| imported | 8 590 | 45,89 |

| manufactured in Russia | 10 127 | 54,11 |

| - supply / upgrade of steam boilers | 18 230 | 100,00 |

| including: | ||

| imported | 8 180 | 44,87 |

| manufactured in Russia | 10 050 | 55,13 |

* – Analysis performed based on current data of OGK and TGK for completed and current investment projects involving commissioning of 90 new and upgraded (reconstructed) TPP units in 2010-2017Analysis is an estimate.

All those factors have a significant impact on the market of pipe valves, which is a tough competitive environment for Russian manufacturers active on the market of new construction and repair and maintenance.It has to be stressed that the situation on the market of new construction is not in favor of Russian companies.Russian power engineering industry has lost its leading position and in terms of key equipment its products have been largely replaced by those by Siemens, Alstom, Ansaldo, GeneralElectric, Harbin plants, etc.

All these features have an impact on the current requirements to the valve market for thermal power plants:

- Value for money ratio shifts in favor of low prices at the minimum sufficient level of quality, especially in the market of spare parts and functionally simple valves (gate valves, stop valves and check valves, gates).

- Increased reliability of functionally complex valves (safety, control, reducer and cooling units).

- Use of more heat-resistant, corrosion-resistant steel grades compared to traditionally used in piping systems.

- Working environment parameters becoming more challenging – from supercritical (up to 580˚C) to ultra supercritical (over 600˚C).

Expert assessment of the average annual market demand for valves of the Russian thermal energy industry is RUB 12 bn.

Nuclear power

Russian nuclear power industry, unlike the conventional power, preserves and continues to develop its scientific and industrial potential.Adoption in 2006 of the Federal Target Program (FTP) “Development of the Nuclear Industry of Russia in 2007-2010 and till 2015” became the basis for the strategic development of the nuclear power industry.

Today, 33 units at 10 nuclear power plants are operated in Russia.Roadmap of construction of new units in the medium term provides for commissioning of additional 8 units.

Figure 1. Schedule of planned commissioning dates of NPP units

Russian nuclear industry demonstrated its world class by exporting nuclear power technology to many countries around the world – China, India, Vietnam, Turkey, Finland, Hungary, Bangladesh, Czech Republic, Slovakia, Belarus.

Analysis of the implementation of FTP and roadmap shows that the actual annual demand for power engineering valves for new NPP projects is one complete unit VVER-1000/1200, which in real terms is about 27,697 pieces of equipment (using as an example Unit 3 of Rostov NPP (VVER-1000 design V-320)).

Table 2. Pipe valves used in Unit 3 of Rostov NPP

| № | Item, body part material grade | Quantity |

|---|---|---|

| 1 | Gate valves, including: | 2 162 |

| Stainless steel | 283 | |

| Carbon steel | 1 862 | |

| Cast iron | 17 | |

| 2 | Gates | 936 |

| 3 | check gates, including: | 351 |

| Stainless steel | 145 | |

| Carbon steel | 133 | |

| Other materials (cast iron, etc.) | 73 | |

| 4 | Pilot operated relief valves (excl. steam generator pilot operated relief valves) - stainless steel | 20 |

| 5 | Stop valves, including: | 19 762 |

| Stainless steel | 11 204 | |

| Carbon steel | 6 089 | |

| cast iron, aluminum, bronze, etc. | 2 470 | |

| 6 | Check valves, including: | 447 |

| Stainless steel | 207 | |

| Carbon steel | 147 | |

| cast iron, aluminum, bronze, etc. | 93 | |

| 7 | safety valves | 254 |

| 8 | control valves, including | 347 |

| Stainless steel | 162 | |

| Carbon steel | 112 | |

| cast iron, aluminum, bronze, etc. | 73 | |

| 9 | ball valves | 1 623 |

| 10 | other fittings | 1 795 |

| TOTAL, including: | 27 697 | |

| Class 2 | 7 850 | |

| Class 3 | 4 871 | |

| Class 4 and unclassified | 14 976 |

General requirements to nuclear power plant valves:

- full compliance with rules and regulations in the nuclear industry,

- reliability,

- referentiality (conservatism)

- lowest price.

In our opinion, the value for money relationship is currently dominated by price at the minimum required level of quality.This factor leads to the fact that valve manufacturers have almost stopped investing resources in product development, which in turn makes Russian products less competitive in the construction of nuclear power plants abroad and creates the preconditions for increasing the share of imports in the construction of nuclear power plants in Russia. For example, in the construction of Units 1 and 2 at Tianwan NPP in China, the degree of the customer’s distrust in the possibility of procuring special valves from Russia was less than 10% (estimate by Atomenergoproekt, St. Petersburg), but in the construction of Units 3 and 4 of the same NPP, the customer’s distrust (in other words, localization) rose to 50% of the total scope of supply of valves.Only two companies – Mechanical Engineering Corporation Splav, Veliky Novgorod, and CKBA, Kiev, were approved by the Chinese customer to enter into direct contracts for the supply of valves for the new units of Tianwan NPP.

Table 3.Changes in the composition of manufacturers of valves for Tianwan NPP, China

| Manufacturers of valves for Phase 1 of TNPP (Units 1 and 2)ТАЭС (блоки №1 и №2) | Manufacturers of valves (similar product range) for Phase 2 of TNPP (Units 3 and 4) |

|---|---|

| OAO Mechanical Engineering Corporation Splav | OAO Mechanical Engineering Corporation Splav, DalianDVValveCo.,Ltd, China |

| OAO Chekhov Power Engineering Plant | Sempell GmbH, Germany Sufa Technology Industry Co., Ltd.China CKBA Kiev, Ukraine |

| MSA a.s.Czech Republic | Sempell GmbH, Germany Sufa Technology Industry Co., Ltd.China CKBA Kiev, Ukraine |

| Mostro a.s.Czech Republic | Sempell GmbH, Germany |

| ZAO Znamya Truda | Sufa Technology Industry Co., Ltd.China CKBA Kiev, Ukraine |

| OAO Saturn | Sufa Technology Industry Co., Ltd.China CKBA Kiev, Ukraine |

| ZAO Firma Soyuz-01 | ZAO Firma Soyuz-01 |

| OAO Penztyazhpromarmatura | OAO Penztyazhpromarmatura |

| OAO Ivano-Frankovsk Valve Plant, Ukraine | Sufa Technology Industry Co., Ltd.China CKBA Kiev, Ukraine |

| ZAO NPF CKBA | Sufa Technology Industry Co., Ltd.China CKBA Kiev, Ukraine Velan, Canada-France |

| OAO Ikar | Sufa Technology Industry Co., Ltd.China |

The degree of localization in the future contract for the construction of Phase 2 of Kudan-Kulam NPP in India is 30% of the combined equipment; it is highly likely that in respect of pipe valves this figure can rise to 60%.Although it should be noted that there are no fundamental design differences between Phase 1 (Units 1 and 2) and Phase 2 (Units 3 and 4) of Kudan-Kulam NPP, preferences of manufacturers in installation, testing and operation of Phase 1, availability in India of own valve manufacturers are likely to lead to a 2 times reduction in the supplies of Russian valves and fittings.

Besides, there is another negative factor for Russian valve manufacturers: nuclear power plants in Kaliningrad Region and in Turkey (VVER-TOI design) will use turbines by Alstom, which means that classified valves for the turbine hall will be manufactured outside Russia (in France, Germany , Canada, Spain, Czech Republic).That is, there is a tendency of procuring imported valves for Russian projects.What this leads to is clearly illustrated by Phase 2 of Tianwan NPP; in thermal energy, the share of imported valves is up to 55% in the construction of new units in Russia

In the development of the evolutionary VVER-TOI project, there was an engineering trend directly related to power engineering valves.It was the use in piping systems (pipes + valves), instead of carbon steel grades, pearlite and martensitic steel grades with high yield point at 250˚C and high corrosion resistance.

In recent years, in the operation of nuclear power plants the transition from routine maintenance of equipment to operation and maintenance of equipment based on its actual condition has become relevant.For valves, primarily those with electric drives, as the most representative of class of equipment, this problem is reflected in additional requirements to diagnostic equipment, development of diagnostic parameters and processing methods.Given that this is a global trend, valve manufacturers also need to reconsider their attitude to this problem in the design, manufacture, testing of their products and the development of special methods.

Based on the findings of market research conducted by the Central Scientific Research Design Institute for Modern Technologies in the Valve Engineering Industry in cooperation with the Research and Industry Association of Valve Manufacturers, average annual market demand for valves for nuclear power plants in Russia (incl. demand for spare parts) is estimated at RUB 3.7 bn.

Analysis of the valve market for power engineering

As mentioned at the beginning of this report, valve market development depends on the state of the demand industry (power generation) and of the supply industry (mechanical engineering).It would be incorrect to apply strictly sectoral analysis to valve manufacturers (manufacturers of valves for nuclear power plants and thermal power plants), since the majority of companies are diversified in terms of markets (nuclear and thermal power, oil, gas, petrochemical, and other applications) and functional purpose of valves.In addition, the majority of businesses are part of holding companies – both diversified and non-diversified, which also prevents the principle of sectoral analysis from being fully applied.

It is proposed to carry out a comparative analysis of the two groups of companies, both Russian and foreign, operating on the Russian market of consumption and production, by the criterion of export potential as integral index of competitiveness.

One of the main criteria of efficiency of the company, its competitiveness, is its export potential, that is, the set of available resources and opportunities for the production of competitive products, their sales and maintenance in foreign markets, both in the short and long term.Unfortunately, we have to acknowledge that the export potential of Russian companies is vanishing.

In nuclear power, because of the tendency of localization of production in the countries of Russian exports, this figure has decreased almost 2 times.In addition,it should be noted that this is not purely export potential of Russian valve manufacturers, but the potential of the Russian nuclear project as a whole.

In thermal power, exports to foreign countries are approaching zero and decreasing to the former Soviet Union republics – Belarus, Kazakhstan (replaced by supplies from China and South Korea), Ukraine (replaced by supplies from the Czech Republic, Germany, China), Central Asia (replaced by supplies from Western Europe, USA, China).

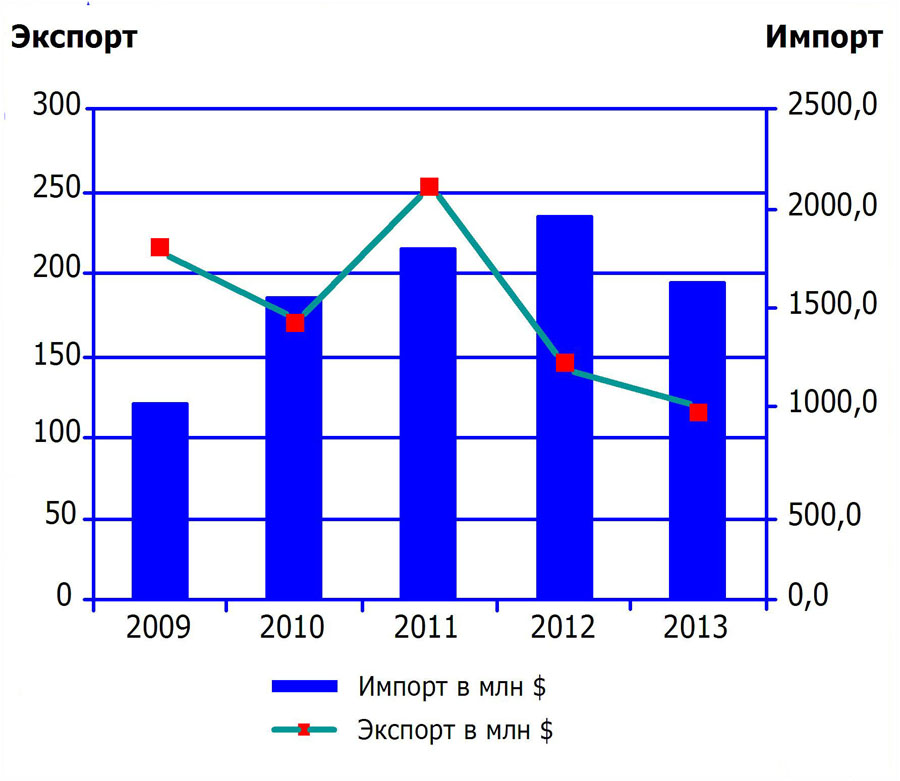

The analytical review “Russian valve engineering in 2013”, prepared by the Research and Industry Association of Valve Manufacturers, shows the dynamics of imports and exports of pipe valves in general.

Figure 2.Dynamics of imports and exports of pipe valves in Russia

From the above chart it follows that Russian valve industry is losing its market position both in Russia and in other countries.Imports of valves in absolute terms exceed exports by more than 10 times.In the energy sector, this ratio looks certainly more optimistic, especially in nuclear power (here the ratio is close to 1:1).However, in new projects in thermal energy imports exceed exports by more than 15 times.

Why is this happening?What can be done?Answers to these questions are not simple and involve many factors, but we will try to analyze some obvious reasons for the dynamics of this lag.

- Lack of complete, integrated and, more importantly, objective analysis of the competitiveness of Russian companies.

- General technical backwardness in the field of new energy technologies, as the main driver of new properties and capabilities of valves for power engineering. Backwardness in the development of combined-cycle technology – leading Western countries are building 4th generation plants, while Russia has implemented only combined-cycle plants of the 1st generation.

- The decline of Russian power engineering in terms of production of equipment packages for turnkey construction of thermal power plants and the substitution of Russian-made turbines and boilers with those by leading Western (and not only Western) manufacturers – Siemens, Alstom, Ansaldo, GeneralElectric, Harbin Turbine and Boiler Plants, etc.

- Underestimating the need for an integrated development of the technological capacity of the company.We use the tactics of intensive development of machining technology and to a lesser degree of control and test technologies, surface hardening processes (deposition welding, chemical and heat treatment, etc.).

- Underestimation of the need for actual implementation of technical standards from other countries, European directives on safety (DIN, ASME, ASTM, ISO, PED, etc.) to enter regional markets.

- Lagging of iron and steel industry in the manufacture of body pieces that meet up-to-date requirements to continuity, short-term and long-term mechanical properties, precision of workings, narrow choice of commercially available steel grades.Western manufacturers can use in their designs more resistant and corrosion-resistant steel grades and have 2 times more application options.In Russia, the choice of steel grades for body parts of power engineering valves is mainly confined to the following grades – 20, 15GS, 12H1MF, 15H1M1F; while, for example in Germany, valve manufacturers can choose from steels 1.0460, 1.5415, 1.7335, 1.7380, 1.4303, 1.0566, 1.6368, 1.4550.

- Accumulated subjective dissatisfaction in power engineering with Russian-made valves in long-term operation, on the one hand, and “waiting for a miracle” from imported valves (looks nice and have not yet tried in operation), on the other hand.

- Lack of a comprehensive system of training professionals in various fields of the valve industry.

- Fierce competition between Russian manufacturers and the virtual absence of competition with Western manufacturers, especially in their traditional markets.

The answer to the question “who is to blame?” is to a large extent – “we ourselves” (and not the reasons mentioned above).

What can be done?

We need to do same things that our competitors do, but on a larger scale and at a higher rate, because they are already in a more advanced position:

- We should have a detailed comprehensive plan for the strategic development of the company, based not only on ambitious goals, but most importantly on a realistic assessment and findings of competitiveness analysis of the company and its products.

- Develop programs for becoming certified and listed as approved suppliers to major Russian and foreign customers of valve products (OAO Power Machines, OAO ZIO Podolsk, OAO Atomenergomash, Siemens, GeneralElectric, Ansaldo, Alstom etc.).

- We have to realize that Russian valve manufacturers should not only compete against each other, but also share their resources and capabilities to address common technological, structural and organizational challenges:

– development of a methodological program for implementation of basic international standards in energy (if necessary, an ad hoc group should be established under Research and Industry Association of Valve Manufacturers another industry organization);

– establishment of specialized training centers for skilled professionals under Research and Industry Association of Valve Manufacturers, conducting periodic specialized training sessions in Russian technical universities;

– development and lobbying of import substitution program for the new generation of high-temperature, erosion and corrosion resistant steels in the form of actual semi-finished products, castings and forgings for piping systems and valves followed by commercialization at modern steel plants;

– development and lobbying of the program to create a modern valve test center.

- Use the platform offered by the interdisciplinary journal not only for informational, educational and promotional purposes, but also to provide objective information about the real feedback on the operation of valve products by Russian and foreign manufacturers at power facilities (for example, VNIIAES reports on valves).

To summarize, we would like to emphasize once again that the market of power engineering valves in Russia has strong growth prospects, but in order to have dominant position on this market and to become real markets participants in other countries, it is necessary to reverse the negative trend in the Russian valve industry.